Last update 23/11/2019

The different IFRS valuation premises are? That is the question and this is the answer.

The different valuation premises available in IFRS and how they are used are:

Stand-alone valuation premise

A basis used to determine the fair value of an asset that provides maximum value to market participants principally on a stand-alone basis.

In combination value

A basis used to determine the fair value of an asset that provides maximum value to market participants principally through its use in combination with other assets and liabilities as a group (as installed or otherwise configured for the highest and best use valuation premise). The different IFRS valuation premises are

The highest and best use valuation premise establishes the valuation premise used to measure the fair value of that asset

Difference between the current use of an asset and the highest and best use valuation premise: The different IFRS valuation premises are

The current use is how the reporting entity is currently using an asset and the highest and best use valuation premise is based on how market participants will use the asset.

An example of where the two may differ is where land is currently used as a site for a factory, but the land could be used for residential purposes. The current use is industrial while the highest and best use could be residential.

Valuation premises are in combination value, stand alone value and highest and best use value. The different IFRS valuation premises are

Guidance on measurement

IFRS 13 provides the guidance on the measurement of fair value, including the following: The different IFRS valuation premises are

- An entity takes into account the characteristics of the asset or liability being measured that a market participant would take into account when pricing the asset or liability at measurement date (e.g. the condition and location of the asset and any restrictions on the sale and use of the asset) [IFRS 13 11]

- Fair value measurement assumes an orderly transaction between market participants at the measurement date under current market conditions [IFRS 13 15]

- Fair value measurement assumes a transaction taking place in the principal market for the asset or liability, or in the absence of a principal market, the most advantageous market for the asset or liability [IFRS 13 24]

- A fair value measurement of a non-financial asset takes into account its highest and best use [IFRS 13 27]

- A fair value measurement of a financial or non-financial liability or an entity’s own equity instruments assumes it is transferred to a market participant at the measurement date, without settlement, extinguishment, or cancellation at the measurement date [IFRS 13 34]

- The fair value of a liability reflects non-performance risk (the risk the entity will not fulfil an obligation), including an entity’s own credit risk and assuming the same non-performance risk before and after the transfer of the liability [IFRS 13 42]

- An optional exception applies for certain financial assets and financial liabilities with offsetting positions in market risks or counterparty credit risk, provided conditions are met (additional disclosure is required). [IFRS 13 48, IFRS 13 96]

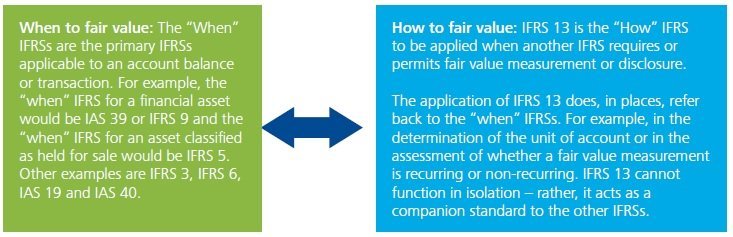

The ‘when’ and ‘how’ of fair value measurement

In terms of where to start in the determination of fair value, it is useful to consider three broad steps that should be taken before delving into the details that inevitably will follow. These steps are important in illustrating the relationship between the primary IFRS that dictates when fair value measurement is required and IFRS 13 which is the “how” IFRS.

Step 1: Identify the balance or transaction that must (may) be measured or disclosed at fair value and when such measurement (disclosure) is necessary.

Step 2: Consult IFRS 13 for guidance on how to determine fair value upon initial recognition.

Step 3: Consult the “when” IFRS to determine if the subsequent measurement of the account balance is at fair value and/or if fair value disclosures are required.

How to determine fair value – key considerations

Once you have established the item that is the subject of fair value measurement (and/or disclosure), the nuts and bolts of IFRS 13 come into play.

The standard could appear overwhelming – it is comprised of 99 paragraphs of core guidance plus a further 47 paragraphs of application guidance (Appendix B to IFRS 13). As you get more familiar with the standard any fear of fair value will likely subside. In the meantime, the table which follows sets out a summary of the key considerations in how to determine fair value under IFRS 13.

|

IFRS 13 requirement |

What to think of it? |

|

Unit of account – The determination of the unit of account must be established prior to determining fair value and is defined as the level at which an asset or a liability is aggregated or disaggregated in an IFRS for recognition purposes. The unit of account is determined under the IFRS applicable to the asset or liability (or group of assets and liabilities) that requires fair value measurement. |

|

|

Market – Fair value measurement under IFRS 13 assumes that a transaction to sell an asset or to transfer a liability takes place in the principal market (or the most advantageous market in the absence of the principal market). The principal market is the market with the greatest volume and level of activity for the asset or liability. The most advantageous market is the market that maximizes the amount that would be received to sell the asset or minimizes the amount that would be paid to transfer the liability, after taking into account transaction costs and transport costs. |

|

|

Market participant assumptions – A fair value measurement under IFRS 13 requires an entity to consider the assumptions a market participant, acting in their economic best interest, would use when pricing the asset or a liability. Market participants are defined as having the following characteristics:

|

|

|

Inputs and valuation techniques – IFRS 13 does not mandate the use of a particular valuation technique(s) but sets out a principle requiring an entity to determine a valuation technique that is “appropriate in the circumstances”, for which sufficient data is available and for which the use of relevant observable inputs is maximized. IFRS 13 discusses three widely used valuation techniques which are: Valuation techniques should be applied consistently from one period to the next. |

|

Special considerations-non-financial assets, liabilities and own equity instruments

|

Layered within the requirements of IFRS 13 are specific considerations related to certain elements of the financial statements. These considerations effectively add an additional dimension to the base requirements of the standard. |

|

|

Non-financial assets (such as items within the scope of IAS 36, IAS 40 and IFRS 5) are subject to a valuation premise referred to as the “highest and best use”. This requires that fair value be determined based on the highest and best use of the asset from the perspective of a market-participant. |

The measurement of non-financial assets at the highest and best use is a significant change from previous guidance and requires judgment to be applied. |

|

Highest and best use must meet certain criterion and barriers limiting the assets ability should be examined to ensure that the asset’s use is:

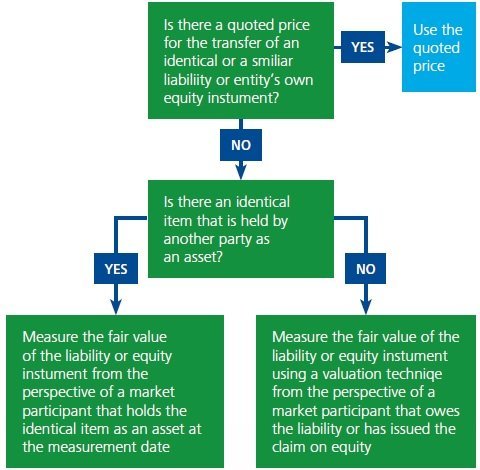

An entity can presume that the current use of an asset is its highest and best use. However, if the asset is being used defensively (e.g. to protect a competitive position), this presumption may be inappropriate. Liabilities and own equity instruments must be measured on the assumption that the liability or equity is transferred to a market participant at the measurement date. This differs (sometimes significantly so) from a measurement that is based on the assumption of settlement of a liability or cancellation of an entity’s own equity instrument. IFRS 13 further requires that the fair value of a liability must factor in non-performance risk. Anything that could influence the likelihood of an obligation being fulfilled is considered a non-performance risk. This could include the risk of physically extracting or transporting an asset or the entity’s own credit risk. |

|

It is important to recognize that the specific approach to fair value liabilities and an entity’s own equity instruments sometimes differs from the concepts to fair value an asset. This is summarized in the decision tree above. |

|

|

The dynamics In today’s financial reporting environment, no IFRS is static. The issuance of other new standards and interpretations can at times prompt a review of aspects of the guidance. Further, it is only after the initial implementation and application of a new standard that some of the practical or interpretative issues are encountered. Items under constant discussion are:

|

|

See also: The IFRS Foundation

The different IFRS valuation premises are?

The different IFRS valuation premises are The different IFRS valuation premises are The different IFRS valuation premises are

The different IFRS valuation premises are The different IFRS valuation premises are The different IFRS valuation premises are