Last update 29/11/2019

Other business models are the business model you arrive at when a financial asset and its handling in a business does to lead to the ‘hold to collect’ or ‘hold to collect and sell’ business models. Financial assets are measured at fair value through profit or loss if they are not held within a business model whose objective is to hold assets to collect contractual cash flows or within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets (but see also IFRS 9 paragraph 5.7.5).

An entity’s business model for managing financial assets:

- reflects how financial assets are managed to generate cash flows

- is determined by the entity’s key management personnel

- does not depend on management’s intentions for individual instruments but is based on a higher level of aggregation that reflects how groups of financial assets are managed together to achieve a particular business objective.

One business model that results in measurement at fair value through profit or loss is one in which an entity manages the financial assets with the objective of realising cash flows through the sale of the assets. The entity makes decisions based on the assets’ fair values and manages the assets to realise those fair values. In this case, the entity’s objective will typically result in active buying and selling.

Even though the entity will collect contractual cash flows while it holds the financial assets, the objective of such a business model is not achieved by both collecting contractual cash flows and selling financial assets. This is because the collection of contractual cash flows is not integral to achieving the business model’s objective; instead, it is incidental to it. Other business models

A portfolio of financial assets that is managed and whose performance is evaluated on a fair value basis (as described in IFRS 9 paragraph 4.2.2(b)) is neither held to collect contractual cash flows nor held both to collect contractual cash flows and to sell financial assets. The entity is primarily focused on fair value information and uses that information to assess the assets’ performance and to make decisions.

In addition, a portfolio of financial assets that meets the definition of held for trading is not held to collect contractual cash flows or held both to collect contractual cash flows and to sell financial assets. For such portfolios, the collection of contractual cash flows is only incidental to achieving the business model’s objective. Consequently, such portfolios of financial assets must be measured at fair value through profit or loss.

Financial assets held in any other business model are measured at FVTPL (except when an entity elects to present in OCI subsequent changes in the fair value of an investment in an equity instrument).

Other business models are all those that do not meet the ‘hold to collect’ or ‘hold to collect and sell’ qualifying criteria. Some examples are:

- assets managed with the objective of realising cash flows through sale; Other business models

- a portfolio that is managed, and whose performance is evaluated, on a fair value basis; and Other business models

- a portfolio that meets the definition of ‘held-for-trading’1. Other business models

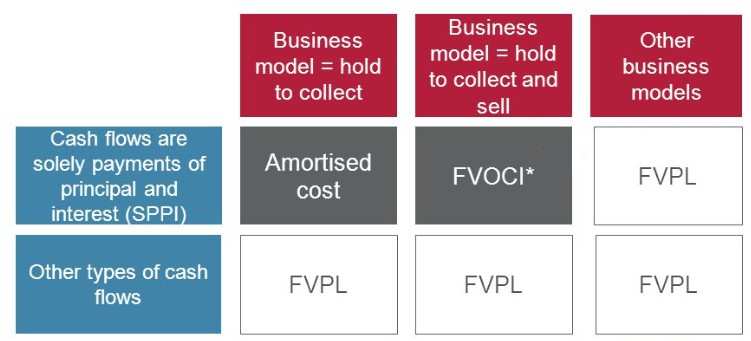

All non-equity financial assets falling into ‘other’ business models must be classified at fair value through profit or loss, irrespective of whether the SPPI test is passed.

* Equity investments can elect for fair value through other comprehensive income

* Equity investments can elect for fair value through other comprehensive incomeWhy is the Business Model assessment important?

The classification decision for non-equity financial assets under IFRS 9 is dependent on two key criteria:

- the business model within which the asset is held (the business model test); and Other business models

- the contractual cash flows of the asset (the Solely Payments of Principal and Interest (SPPI) test) Other business models

Consequently, determining the business model within which the financial asset is held is necessary in order to determine the appropriate classification category under IFRS 9.

See also: The IFRS Foundation