Last update 25/11/2019

IFRS 15 47 provides the requirements to determine the transaction price. The transaction price is based on the amount to which the entity expects to be ‘entitled’. This amount is meant to reflect the amount to which the entity has rights under the present contract (see contract enforce-ability and termination clauses). That is, the transaction price does not include estimates of consideration resulting from future change orders for additional goods or services. Determine the transaction price

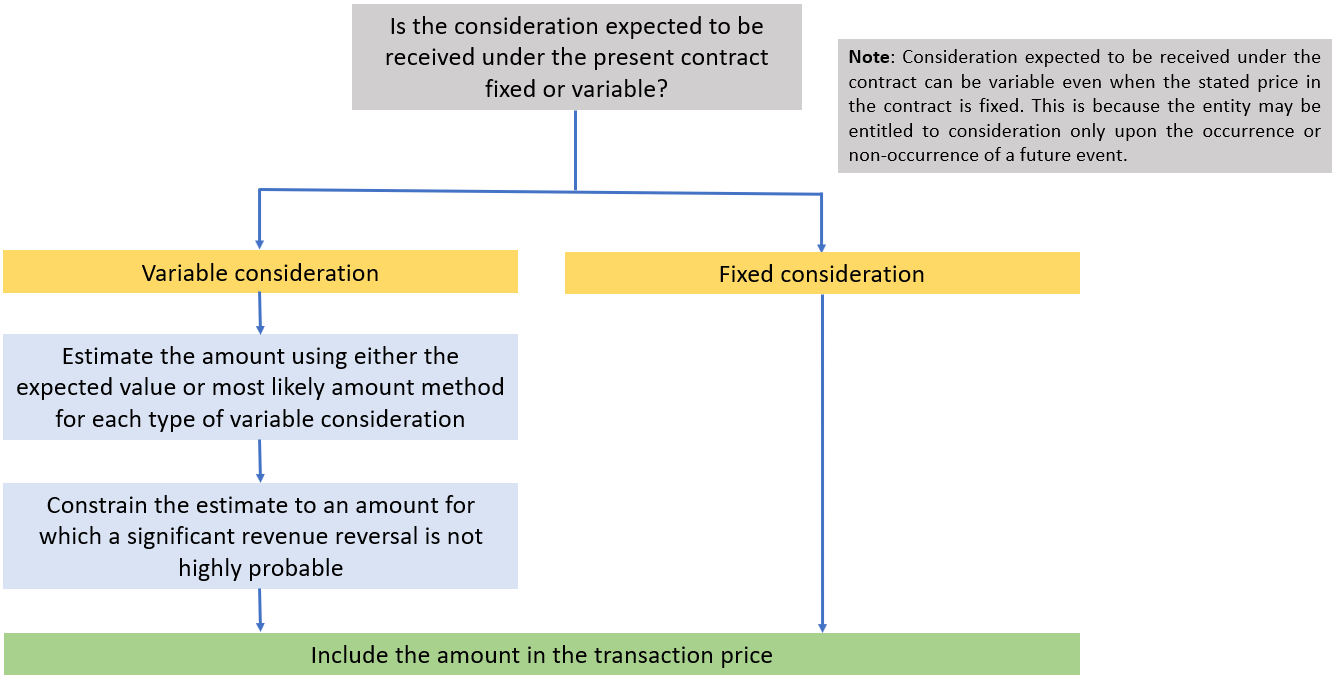

Determine the transaction price

Determining the transaction price is an important step in applying IFRS 15 because this amount is allocated to the identified performance obligations and is recognised as revenue when (or as) those performance obligations are satisfied. In many cases, the transaction price is readily determinable because the entity receives payment when it transfers promised goods or services and the price is fixed (e.g., a restaurant’s sale of food with a no refund policy). Determine the transaction price

Determining the transaction price is more challenging when it is variable, when payment is received at a time that differs from when the entity provides the promised goods or services or when payment is in a form other than cash. Consideration paid or payable by the entity to the customer may also affect the determination of the transaction price. Determine the transaction price

The following flow chart illustrates how an entity would determine the transaction price if the consideration to be received is fixed or variable: Determine the transaction price

References:

- Determining the transaction price – IFRS 15 – 47 – 49

Document your decisions in your financial close file to facilitate internal review and approval and external audits.

Variable consideration

The transaction price reflects an entity’s expectations about the consideration to which it will be entitled to receive from the customer. The standard provides the following requirements for determining whether consideration is variable and, if so, how it would be treated under the model in IFRS 15 50 – 52. Determine the transaction price

- Forms of variable consideration Determine the transaction price

IFRS 15.51 describes ’variable consideration’ broadly to include discounts, rebates, refunds, credits, price concessions, incentives, performance bonuses and penalties. Variable consideration can result from explicit terms in a contract to which the parties to the contract agreed or can be implied by an entity’s past business practices or intentions under the contract. It is important for entities to appropriately identify the different instances of variable consideration included in a contract because the second step of estimating variable consideration requires entities to apply a constraint (as discussed further in section 5.2.3) to all variable consideration.

Many types of variable consideration identified in IFRS 15 were also considered variable consideration under legacy IFRS. An example of this is where a portion of the transaction price depends on an entity meeting specified performance conditions and there is uncertainty about the outcome.

In many transactions, entities have variable consideration as a result of rebates and/or discounts on the price of products or services they provide to customers once the customers meet specific volume thresholds. The standard contains example #24 relating to volume discounts in IFRS 15 IE124 – IE128.

Optional purchases

Contracts frequently include options for customers to purchase additional goods or services in the future. Customer options that provide a material right to the customer (such as a free or discounted good or service) give rise to a separate performance obligation. In this case, the performance obligation is the option itself, rather than the underlying goods or services. Management will allocate a portion of the transaction price to such options, and recognize revenue allocated to the option when the additional goods or services are transferred to the customer, or when the option expires.

The additional consideration that would result from a customer exercising an option in the future is not included in the transaction price for the current contract. This is the case even if management concludes it is probable, or even virtually certain, that the customer will purchase additional goods or services. For example, customers could be economically compelled to make additional purchases due to exclusivity clauses or other facts and circumstances. Management should not include an estimate of future purchases as a promise in the current contract unless those purchases are enforceable by law regardless of the probability that the customer will make additional purchases.

Judgment may be required to identify the enforceable rights and obligations in a contract, as well as the existence of implied or explicit contracts that should be combined with the present contract.

See also: The IFRS Foundation