Last update 28/12/2019

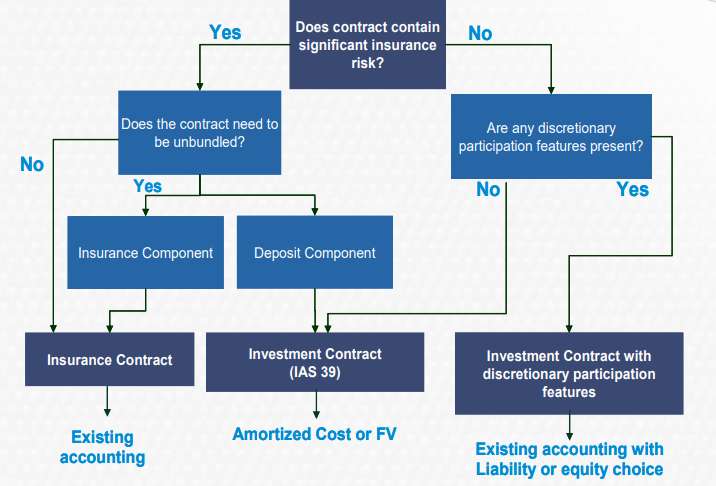

Significant insurance risk – An insurance contract is only in the scope of IFRS 17 if it transfers a significant amount of insurance risk to the entity (or reinsurer).

Insurance risk is only significant if there is at least one scenario with commercial substance where the compensation paid by the insurer is significant, disregarding the likelihood of that scenario. If commercial substance exists only in very unlikely scenarios, but the contract covers all these scenarios, then this qualifies as being significant (see paragraph B18).

Insurance risk can already be significant even if the policyholder still has to opt for insurance cover in the future, but with insurance rates already specified. Also, an insurance contract remains an insurance contract even if the original insurance risk has expired (unless a specified contract modification has occurred.

IFRS 17 requires that the compensation and its commercial substance be considered on a present value basis, unlike IFRS 4, which did not require the use of present values in making this assessment.

Distinction between insurance risk and other risks

- Financial risk: Change in interest rate, security price, commodity price, etc.: NOT insurance risk

- Lapse, persistency or expense risk: NOT insurance risk in direct contract

- Contracts including both financial risk and significant insurance risk have insurance risk

- Must relate to uncertain future event that adversely affects the policyholder

- Must be a pre-existing risk vs. risk created by the contract

Significance test: – Compare:

(1) Cash flows that would be paid if the insured event occurred

Versus

(2) Cash flows that would be paid if no insured event occurred

• Are cash flows under (1) > (2)?

• Are additional benefits significant?

• Does the scenario have commercial substance?

• Evaluated on a contract-by-contract basis

Determining Insurance Risk

Simplified Example of 7 year endowment product. Death benefit equals the endowment benefit.

| Scenario 1 – Policyholder dies in first policy month and received 134k | Scenario 2 – Policyholder survives to endowment and receives 134k, PV = 90k |

Both are insurance risks.

Other illustration: Credit cards that provide insurance coverage

Some credit card contracts may provide insurance coverage and transfer significant insurance risk from the cardholder.

Fact pattern

Credit Card Issuer C provides insurance coverage for purchases that the cardholder makes using the credit card. C would pay the cardholder for claims resulting from a supplier’s misrepresentation or breach of contract. Under this arrangement, C either:

- charges no fee to the cardholder for this service; or

- charges an annual fee that does not reflect an assessment of the insurance risk associated with that individual cardholder.

Analysis

The credit card contract contains both insurance and non-insurance components. This could pose a challenge for C because:

- the requirements in IFRS 17 for separating non-insurance components differ from those in IFRS 4, as explained in the table below; and

- IFRS 4 is less prescriptive about how any insurance component is measured.

| IFRS | Requirements for separating non-insurance components (excluding embedded derivatives) |

| IFRS 4 10-12 | Permits an insurer to separate a loan component from an insurance contract and apply IFRS 9 (or IAS 39) to the loan component. |

| IFRS 17 10 – 13 | Generally requires IFRS 17 to be applied to the whole contract that transfers significant insurance risk.

Separation is permitted only in narrower circumstances than under IFRS 4. Specifically, an insurer separates investment components and goods or non-insurance services components if they are distinct. |

Stakeholders are concerned that credit card issuers that currently account for a loan or a loan commitment in a credit card contract under IFRS 9 (or IAS 39) would need to change the accounting for those contracts that transfer significant insurance risk when IFRS 17 becomes effective – only a short time after having incurred costs to develop a new credit impairment model to comply with IFRS 9.

See also: The IFRS Foundation